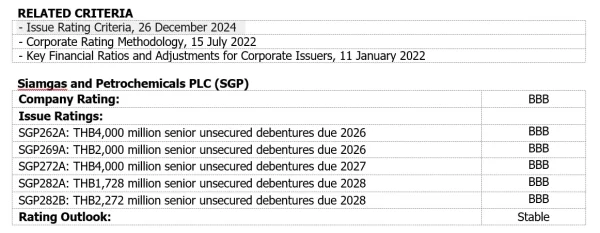

Mitihoon – TRIS Rating downgrades the company rating on Siamgas and Petrochemicals PLC (SGP) and the ratings on its outstanding senior unsecured debentures to “BBB” from “BBB+”. The rating outlook remains “stable”.

The rating downgrade reflects SGP’s weakened financial profile, primarily driven by sizeable capital expenditures and pressures from overseas sales. SGP’s financial leverage will likely remain higher than previously anticipated, with the net debt to EBITDA persistently above our downgrade threshold of 5 times.

The ratings continue to reflect SGP’s solid market position as the second-largest liquefied petroleum gas (LPG) trader in Thailand, along with its significant footprint across several East and Southeast Asian markets. However, the ratings remain constrained by the company’s exposure to volatile LPG prices in international markets. The ratings are also constrained by the company’s potential investment in an LNG import project, which introduces new business risk and could increase financial leverage further.

KEY RATING CONSIDERATIONS

Higher-than-expected capital expenditure

SGP’s financial leverage weakened following capital expenditures totaling THB7.3 billion for three very large gas carriers (VLGCs) and other vessels. The three VLGCs alone accounted for THB6.3 billion, with two delivered in 2024 and the third in May 2025. We had not previously anticipated this scale of investment.

SGP has secured five-year charter agreements for two of the three vessels. The contracts provide fixed monthly income and are expected to deliver high and stable profit margins over their terms. One VLGC commenced operations in July 2024, while the second is set to follow in June 2025. However, even with the projected income from these two VLGC charters, we expect SGP’s elevated debt level to keep its net debt to EBITDA ratio above 5 times.

Lingering headwinds in overseas markets

SGP’s sales outlook remains under pressure, as reflected by a continued decline in sales volume throughout 2024 and into the first quarter of 2025 (1Q25). In 1Q25, total sales volume fell by 10.5% year-on-year (y-o-y), primarily due to a 15.2% drop in overseas sales. This decline highlights prolonged weakness in key overseas markets, particularly China. In contrast, domestic volume continued to grow, increasing by 4.4% y-o-y in 1Q25.

China, SGP’s largest international market, continues to face a supply-demand imbalance driven by an oversupply of local LPG production stemming from subdued demand from the petrochemical sector. This imbalance is expected to persist, exacerbated by ongoing US-China trade tensions, and thus placing pressure on SGP’s operations in the region. Offshore volumes also declined moderately, due to a drop in demand from its large customer in this offshore segment.

Looking ahead, we expect overseas sales volume to remain sluggish over the forecast period. Nonetheless, SGP’s efforts to explore new market opportunities and secure spot orders may help mitigate the risk of further sharp volume contractions.

We forecast total sales volume to decline by 3% in 2025, reaching approximately 3.1 million tonnes, with a gradual recovery to 3.2-3.3 million tonnes annually during 2026-2027.

Second-largest LPG player in Thailand

In the domestic LPG market, SGP maintained a stable market share of approximately 21%-22% in 2024. Its strong domestic position is underpinned by a well-established brand, economies of scale, and extensive nationwide distribution coverage. However, competitive pressure continues to intensify, particularly in the automotive and cooking LPG segments, driven by aggressive pricing strategies among rival players.

Unlike overseas trading, which exhibits greater earnings volatility due to its exposure to LPG price fluctuations, SGP’s domestic LPG operations have provided a relatively steady source of earnings, benefiting from government-regulated pricing and partial subsidies that tend to stabilize profit.

Strong distribution network

SGP’s extensive distribution network serves as a key competitive advantage and reinforces its credit profile. In Thailand, the company operates nine LPG storage terminals, a wide network of filling plants and gas service stations, and a large fleet of LPG trucks and tankers. Internationally, SGP owns two large storage caverns in China with a combined capacity of 300,000 tonnes, along with a fleet of LPG vessels and VLGCs units near Singapore.

These floating storages support SGP’s supply chain flexibility, allowing the company to serve shifting regional demand and capitalize on emerging market opportunities. Additionally, SGP maintains smaller LPG storage facilities in Malaysia, Vietnam, Singapore, and Laos, further strengthening its regional presence and operational scale.

Financial leverage to remain high in 2025 before declining

We project EBITDA to range from THB3.9-THB4.4 billion annually during 2025–2027. Capital spending will likely remain high, with THB3.3 billion slated for 2025, and an average of THB1.7 billion annually during 2026-2027. As a result, net debt to EBITDA is projected to rise slightly above 6 times in 2025, before receding to around 5.3 times by 2027. The ratio of funds from operations (FFO) to debt is forecasted to be around 10%-13%.

Our base case projection does not factor in any potential investment in the LNG import project. Should this investment proceed, it could put some pressure on the credit rating depending on its size and timeline.

Adequate liquidity

We assess SGP’s liquidity position as adequate to meet its debt obligations over the next 12 months. As of March 2025, the company’s available sources of liquidity included approximately THB4.3 billion in cash and cash equivalents, along with estimated funds from operations (FFO) of around THB2.5 billion over the next 12 months. On the liability side, SGP faces long-term loan and lease repayments totaling THB1.1 billion, debenture maturities of THB4 billion, and dividend payments of THB0.37 billion. We expect the company to refinance its maturing debentures through new bond issuances.

Meanwhile, upcoming capital expenditures, primarily related to VLGC procurements, are expected to be largely funded through bank loans. In addition, SGP still holds substantial undrawn credit facilities exceeding THB10 billion, providing ample flexibility to manage short-term debt and liquidity requirements.

Debt structure

At the end of March 2025, SGP had consolidated debt (excluding lease liabilities) of THB24.2 billion. SGP’s priority debt totaled around THB7.9 billion. Hence, the ratio of priority debt to total debt was about 32.5%.

BASE-CASE ASSUMPTIONS

- SGP’s total LPG sales volume to drop to 3.1 million tonnes in 2025, then grow to 3.2-3.3 million tonnes per year during 2026-2027.

- Operating revenue to stay in the THB73-THB75 billion per annum range during 2025-2027.

- EBITDA margin to be around 5.4%-6.0%.

- Capital spending to total THB3.3 billion in 2025 and THB1.7 billion per year during 2026-2027.

- Dividend payout ratio at 40%-50% of net profit.

RATING OUTLOOK

The “stable” outlook reflects our expectation that SGP will maintain its strong market position in the domestic LPG sector, which continues to serve as a reliable source of earnings. We also anticipate that the company will be able to sustain overall LPG sales volumes and deliver EBITDA in line with our projections.

RATING SENSITIVITIES

A rating upgrade could occur if SGP can reduce its net debt to EBITDA ratio to below 5 times on a sustained basis. This improvement may result from successful navigation of overseas market challenges, enhanced EBITDA from both LPG and/or non-LPG segments, and more disciplined investment decisions.

Conversely, downward rating pressure could emerge if the company’s financial profile deteriorates further, with the net debt to EBITDA ratio rising above 7 times. This scenario could be triggered by a failure to maintain LPG sales volumes or large-scale debt-funded investments.

COMPANY OVERVIEW

SGP engages in the LPG trading business in Thailand under the “Siam Gas” and “Unique Gas” brands. The company was established by the Weeraborwornpong family in 2001 and listed on the Stock Exchange of Thailand (SET) in 2008. The family held approximately 55.7% of SGP’s total shares as of March 2024.

SGP’s LPG trading business expanded abroad in 2010 with an aim to increase volumes to offset dwindling demand in the domestic market. Revenue from the international LPG trading segment rose continually, and currently accounts for about 70%-80% of total revenue. In 2023, SGP sold around 3.6 million tonnes of LPG, comprising domestic sales volume of 0.8 million tonnes and international volume of 2.8 million tonnes.

SGP diversified into power generation in 2016. Currently, SGP holds a 41.1% share of a gas-fired power plant in Myanmar with a production capacity of 230 megawatts (MW). The company has also invested in a 33% share of a 10-MW diesel-fired power plant in Myanmar.

In early 2020, SGP completed the acquisition of a 99.69% share of Thai Public Port Co., Ltd. (TPP). TPP, which has been renamed Siam Tank Terminal Co., Ltd. (STT), engages in rental services for oil tank storage, with facilities located at Si-Chang deep seaport in Chonburi Province. In August 2020, SGP purchased 70% shares of Linh Gas Cylinder Co., Ltd. (LINH), an LPG cylinder producer. In early 2021, SGP completed the takeover of LINH, increasing its stake to 97.5%. In 2022, SGP acquired Prasansack Gas Sole Co., Ltd., which operates LPG trading in the Lao People’s Democratic Republic (Lao PDR).

ติดตามช่องทางมิติหุ้นเพื่อรับข่าวสารตลาดทุนได้ตามลิงค์ด้านล่าง

Web : https://www.mitihoon.com/

Facebook : https://www.facebook.com/mitihoon

Youtube : https://www.youtube.com/@mitihoonofficial7770

Tiktok : www.tiktok.com/@mitihoon

ขับเคลื่อนกลยุทธ์ ESG สู่ความยั่งยืน")

THAI หุ้นสุดสตรองสายการบิน ผู้โดยสารพุ่ง-คุมเข็มต้นทุน")

THAI หุ้นสุดสตรองสายการบิน ผู้โดยสารพุ่ง-คุมเข็มต้นทุน")