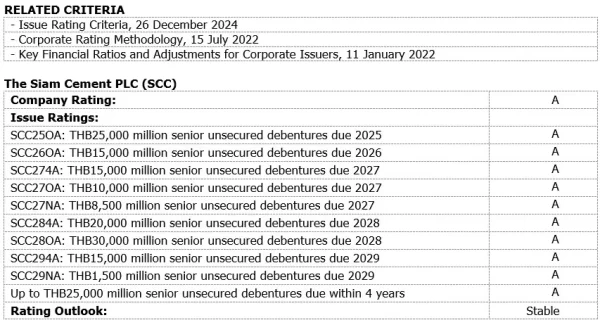

Mitihoon – TRIS Rating assigns a rating of “A” to The Siam Cement PLC’s (SCC) proposed issue of up to THB25 billion senior unsecured debentures, with a tenor of up to four years. SCC intends to use the proceeds from the new debentures to refinance maturing debt. At the same time, we affirm the company rating on SCC at “A” and the ratings on its existing senior unsecured debentures at “A”. The rating outlook remains “stable”.

The ratings mirror SCC’s established presence, prominent market position, as well as diversified business and customer base. These strengths are held back by the prolonged chemicals downcycle and heightened gearing from recent extensive expansion.

We anticipate SCC’s performance improvement, with annual EBITDA increasing to THB53-THB55 billion during 2025-2026 and THB60-THB65 in 2027, from a gradual recovery in its three business segments: Cement-Building Materials (CBM), packaging, and chemicals. Financial leverage will likely remain steady throughout the forecast periods, with the debt to EBITDA ratio at 5-6 times and the funds from operations (FFO) to debt ratio at 10%-13%. We expect the company’s sources of cash, relationships with banks, and ability to tap capital markets to ensure sufficient liquidity.

As of March 2025, SCC’s consolidated debt was about THB318.8 billion, which included priority debts of about THB174.5 billion, most of which were debts at the subsidiary level. This translated to a priority debt to total debt ratio of roughly 55%. Despite exceeding our priority debt threshold of 50%, we rate SCC’s senior unsecured debentures at the same level as the company rating. This is because we anticipate the priority debt ratio to drop below 50%, given SCC’s plan to refinance its subsidiaries’ debts. We also expect SCC to keep the ratio below 50% over the long term.

RATING OUTLOOK

The “stable” outlook reflects our expectation that SCC will remain a leading regional player and perform largely in line with our forecast. The industry diversification should lessen the effects of the chemicals sector downturn. Also, we expect SCC to be cautious with its capital expenditures and follow through on its deleveraging plan.

RATING SENSITIVITIES

A rating upgrade is unlikely to occur within the next 12-18 months. Conversely, a negative rating action may be considered if SCC’s operating performance or financial position deteriorates significantly beyond our base-case forecast. This could result from slower-than-anticipated earnings recovery or more aggressive capital expenditures than projected.

ติดตามช่องทางมิติหุ้นเพื่อรับข่าวสารตลาดทุนได้ตามลิงค์ด้านล่าง

Web : https://www.mitihoon.com/

Facebook : https://www.facebook.com/mitihoon

Youtube : https://www.youtube.com/@mitihoonofficial7770

Tiktok : www.tiktok.com/@mitihoon