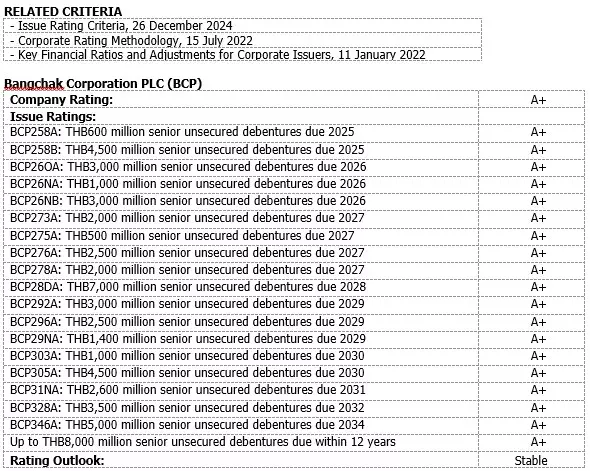

Mitihoon – TRIS Rating assigns a rating of “A+” to Bangchak Corporation PLC’s (BCP) proposed issue of up to THB8 billion senior unsecured debentures, due within 12 years. BCP intends to use the proceeds from this issuance to refinance existing loans and debentures. At the same time, TRIS Rating affirms the company rating and the ratings on BCP’s outstanding senior unsecured debentures at “A+”. The rating outlook remains “stable”.

The ratings continue to reflect BCP’s strengthened business profile following the successful integration of its oil refinery and marketing (R&M) operations, along with expansion in its upstream petroleum exploration and production (E&P) activities. The ratings also consider the benefits of vertical integration in the petroleum sector and the company’s diversified investment. However, the ratings are weighed down by BCP’s susceptibility to volatility in oil prices and gross refining margin (GRM), as well as the execution risk associated with its upcoming projects.

For the first three months of 2025, BCP’s financial performance was in line with our forecast. BCP reported EBITDA of about THB13.3 billion, dropping by 9.1% year-on-year. The debt to EBITDA ratio was 2.9 times (annualized with trailing 12 months). The drop in EBITDA was mainly due to economic slowdown and declined oil prices, putting pressure on the company’s GRM. The sales volumes in the petroleum exploration and production (E&P) business also reduced following the divestment of Yme oil field.

We believe BCP’s strategic initiatives, such as unlocking the synergy benefits from acquiring Bangchak Sriracha PLC (BSRC), enhancing logistics efficiency, and driving corporate cost savings, will be crucial in sustaining earnings and mitigating external pressure. We view the company’s operating environment as challenging due to global trade tensions, a subdued economic outlook, and ongoing geopolitical uncertainties. We expect these strategic efforts to support BCP’s financial performance and keep it aligned with our projections.

As of March 2025, BCP’s consolidated debt, excluding financial lease, was THB127.3 billion while BCP’s priority debt totaled THB61.3 billion, entirely comprising debt owed by its subsidiaries. The ratio of priority debt to total debt was 48.2%.

RATING OUTLOOK

The “stable” outlook reflects our expectation that BCP will perform in line with our projections. Given the company’s plans to improve operational efficiency, we expect BCP’s earnings and financial leverage to align with our estimates, with its debt to EBITDA ratios staying below 3.5 times.

RATING SENSITIVITIES

The potential of an upward revision to the ratings is limited over the near term. Conversely, a downward revision to the ratings could occur from a material deterioration in BCP’s financial risk profile. This could happen if the company’s operating performance falls significantly short of our estimates, or if the company engages in aggressive debt-financed investments or acquisitions.

ติดตามช่องทางมิติหุ้นเพื่อรับข่าวสารตลาดทุนได้ตามลิงค์ด้านล่าง

Web : https://www.mitihoon.com/

Facebook : https://www.facebook.com/mitihoon

Youtube : https://www.youtube.com/@mitihoonofficial7770

Tiktok : www.tiktok.com/@mitihoon