Mitihoon – KTC and its subsidiaries announced a net profit for the year 2025 of 7,782 million Baht, a 4.6% increase from year 2024, reflecting robust credit management strategies and digital transformation. Both revenue and profit grew consistently, supported by a total portfolio of 1.12 hundred billion Baht and the NPL ratio within the target rate. Amidst credit card spending growth that continues to outperform the industry. KTC Group is still committing to its digital strategy, focusing on enhancing customer experience, maintaining asset quality, and expanding its membership base during the economic slowdown.

Mrs. Pittaya Vorapanyasakul, President & Chief Executive Officer of “KTC” or Krungthai Card Public Company Limited, stated, “Even though the overall consumer finance industry contracted due to economic uncertainty and consumers becoming more cautious on spending, KTC Group’s market share over the past 11 months (January-November 2025) increased from the same period in year 2024. The credit card spending had a market share of 13.6% from 13.1% while the credit card receivables compared to the industry had a market share of 14.9% from 14.3% and the personal receivables (excluding car title loans) compared to the industry had a market share of 4.2% from 4.1%.”

“Year 2025 was another challenging year due to the economic slowed down continuously. However, KTC Group still generated higher net profit than the previous year, meeting its targets and reflecting strong operational performance, efficient management, and excellent asset quality control. In year 2026, we are ready to move forward by strengthening our portfolio, continuously increasing the value and rationality of credit card spending for our members, coupled with investing in digital technology by implementing a new core system to increase flexibility and enhance customer experience. The core system also supports the growth of two core businesses, credit card and personal , with the potential to expand into the insurance brokerage business for sustainable revenue.”

“The Group still places an importance on conducting business prudently and closely monitoring various situations to effectively manage risks across all aspects by utilizing data and advanced analytic system to maintain quality and long-term financial stability. It is anticipated that net profit of year 2026 will exceed that of year 2025, with total portfolio growth of approximately 1-2%, NPLs ratio not exceeding 2%, credit card spending growth of 5%, and personal portfolio growth of 2%. However, if the Thai economy is strong in 2026, KTC Group believes that its business can grow even better than projected.”

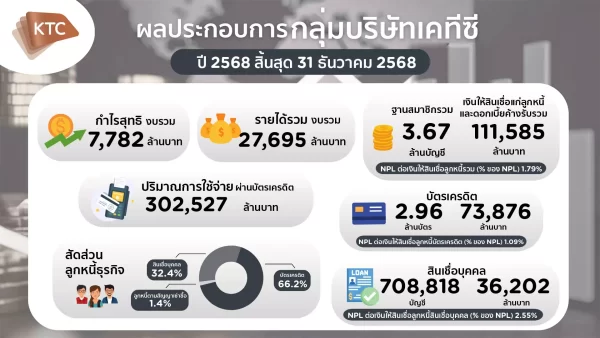

As of December 31, 2025, the KTC Group reported a total membership base of 3,673,244 accounts. Loans to customers and accrued interest stood at Baht 111,585 million, representing a 0.4% year-on-year increase. The non-performing loan ratio (%NPL) remained well-controlled at 1.79%. Credit card accounts totaled 2,964,426 cards (up 5.9% YoY), with receivables of Baht 73,876 million (down 0.1% YoY). Total credit card spending for 2025 grew 3.6% YoY, while the credit card %NPL was maintained at 1.09%. Personal loan accounts reached 708,818 (up 2.9% YoY), and the combined personal loan portfolio—including KTC P BERM (Car for Cash)—amounted to Baht 36,202 million, increasing 3.2% YoY. The %NPL for personal loans was 2.55%. For the KTBL business, KTC has suspended new lending since August 2023 and continues to focus on debt collection and managing the quality of the existing portfolio.

As of December 31, 2025, the KTC Group reported a total membership base of 3,673,244 accounts. Loans to customers and accrued interest stood at Baht 111,585 million, representing a 0.4% year-on-year increase. The non-performing loan ratio (%NPL) remained well-controlled at 1.79%. Credit card accounts totaled 2,964,426 cards (up 5.9% YoY), with receivables of Baht 73,876 million (down 0.1% YoY). Total credit card spending for 2025 grew 3.6% YoY, while the credit card %NPL was maintained at 1.09%. Personal loan accounts reached 708,818 (up 2.9% YoY), and the combined personal loan portfolio—including KTC P BERM (Car for Cash)—amounted to Baht 36,202 million, increasing 3.2% YoY. The %NPL for personal loans was 2.55%. For the KTBL business, KTC has suspended new lending since August 2023 and continues to focus on debt collection and managing the quality of the existing portfolio.

Total revenue for the year 2025 equaled to 27,695 million Baht, slightly increased by 0.9% (YoY), while total expenses decreased by 5.23% (YoY) equaled to 17,239 million Baht mainly due to a reduction in expected credit losses (ECL) resulting from effective asset quality management, as well as lower financial costs driven by reduced borrowings and a lower cost of funds. Operating expenses rose slightly, driven by marketing expenses from promotional campaigns aimed at stimulating credit card spending and new member acquisition. As a result cost to income ratio of 34.8%, a slight improvement from 35.0%.

In terms of asset quality, the Group continues to maintain strong and sufficient reserves. The credit cost for 2025 was 5.3%, a decrease compared to 6.1% in the same period of last year.

The Group had short-term available credit line of THB 20,470 million. Over the same period, debentures and long term borrowings maturing in 2026 amounted to THB 15,830 million. Available liquidity therefore exceeds near term debt obligations, reflecting a strong liquidity position and a very low risk of short term refinancing or default.

Mrs. Pittaya mentioned the progress of the insurance brokerage business (non-life and life insurance), stated “the Group has commenced the insurance brokerage operations by collaborating with non-life and life insurance partners to offer a wide variety of insurance products through KTC’s channels to credit card and personal loan customers. The Company focuses on integrating technology to meet members’ needs more precisely while enhancing services and ensuring secure, privacy-conscious customer data management. This strategic initiative aims to create new business opportunities and increase fee-based income from insurance product offerings. The Company plans to grow this business gradually and prudently, contributing to enhanced service value for customers and generating additional income for the Company”.

KTC Group continues to implement long term debt relief measures in line with the Bank of Thailand’s Notification No. 3/2025 on Responsible Lending. KTC assesses each customer’s credit application based on individual repayment capacity, ensuring that new credit does not impose an excessive additional burden beyond existing obligations. Further details on these measures are available on the Company’s website, https://www.ktc.co.th/about/news/measure. As a non-bank financial institution within the Krungthai Bank Group, KTC has actively cooperated with the Bank of Thailand by participating in both Phase 1 and Phase 2 of the “You Fight, We Help” program. The initiative aims to support vulnerable debtors in restoring their repayment capacity and ultimately settling their obligations once income recovers. Registration for the program closed on September 30, 2025.

Moreover, in situations where customers are affected by natural disasters, such as flooding in southern Thailand, KTC implements relief measures, including reductions in minimum payment requirements and installment amounts. Affected customers may apply for these measures to ease their financial burden and facilitate a faster recovery. Recently, the Group has joined the “Clear Debt, Move Forward” program, under which KTC will transfer and sell unsecured non-performing retail loans overdue for more than 90 days (NPL), based on borrower’s status as of September 30, 2025. Eligible debtors are those with total NPL exposure across all financial service providers and all loan types not exceeding THB 100,000 per person. These receivables will be transferred to Sukhumvit Asset Management Company Limited (SAM) for debt restructuring under more accommodative terms and for the reduction of borrowers’ debt burdens. Registration for the program will be available through channels of the Bank of Thailand starting January 5, 2026.

KTC Group assesses that participation in these programs, as well as the aforementioned debtor assistance measures, will not have a material impact on the Group’s overall operating performance. In this regard, the Company has already established adequate allowances for doubtful accounts.

ติดตามช่องทางมิติหุ้นเพื่อรับข่าวสารตลาดทุนได้ตามลิงค์ด้านล่าง

Web : https://www.mitihoon.com/

Facebook : https://www.facebook.com/mitihoon

Youtube : https://www.youtube.com/@mitihoonofficial7770

Tiktok : www.tiktok.com/@mitihoon